Yen Carry Trade

There has been a lot of talk recently about the Yen carry trade, and how it has gone tremendously wrong for a lot of participants, with some arguing it aided the massive stock market selloff we witnessed in the first week of August. Unfortunately, as with a lot of financial discussions, people tend to assume that everyone is an expert in these matters and so their explanations miss out on some of the finer details. I like to think I have a knack for taking a complex subject and breaking it down so that everyone can understand, so here is my attempt at not just explaining this trade, but how traders could have used FX hedging to better mitigate the risks that caused the recent losses.

The Yen carry trade is relatively simple at its core. Since 2010 the Japanese government has kept central bank interest rates at 0% as they looked to stimulate the economy and encourage inflation. In fact from 2016 until 2024 rates were actually negative at -0.1%. This means that you could borrow Yen over short or longer-term time periods at zero cost. If you borrowed 1,000,000 Yen for 1 year, when you paid it back you would still only owe 1,000,000 Yen. In fact, at negative rates you’d owe slightly less than you borrowed - imagine being paid to take someone’s money!

Here is where the opportunity for global investors came in. Post-covid, when the US federal funds rate started increasing, there became a large arbitrage opportunity. Investors could borrow Japanese Yen, convert it into US dollars, buy extremely safe government bonds at 3%, then 4%, then 5% yields, then when they received the much higher US interest, convert the USD back into JPY and repay the Yen loan, profiting from the difference in interest rates.

For those investors who were looking to take more risk, instead of buying bonds or other essentially guaranteed investments, they could invest in stocks that had the potential to deliver much higher returns than 5%.

Another factor these investors had going for them was that over the last 5 years, there has been a fairly steady appreciation in the USD/JPY foreign exchange rate. This means that along with capturing the difference between US and Japanese interest rates, they were also profiting from a better FX rate when they repaid the Yen loan. They initially sold Yen and bought dollars, then when they went to sell the dollars they were worth more Yen than they originally sold.

The below table is a generic example of borrowing Yen to buy $1m of a 5% returning bond, using an FX rate that remains constant throughout the period of the loan.

5% bond return

The investor has profited $50k USD on this trade, using borrowed money.

The next table is a realistic example of borrowing Yen to buy $1m of a 5% returning bond in January 2023 on a 1-year time frame and what the resulting P&L would have looked like.

5% bond return including FX profits

As you can see from the table, this trade garnered an almost 19% return in a year, not bad for using someone else’s money.

So what happened recently that caused so much panic and discussion to bring this trade to the forefront of the news cycle? The Japanese central bank raised the cost of borrowing for only the 2nd time in 17 years, to 0.25%. Now for those of you who had to get a mortgage in the last few years, 0.25% still sounds like a dream rate! However, markets are forward-looking and the tone from Japan that was broadcast to the market was that the era of ‘free’ money is coming to an end. The Japanese announcement happened to coincide with the US Fed signaling that interest rate cuts are coming in the US. Typically when one government is raising rates, and another government is cutting them, the FX rate is going to be impacted. This is exactly what happened and the USD/JPY rate went from a high of 160 in July to 146.5 at the beginning of August.

Let’s look at that same carry trade, borrowing Yen to make a $1m investment in the US with a return of 5%, but this time a starting FX rate of 160 and a rate of 147 when repaying the loan:

5% bond return subtract FX loss

This trade, despite the positive difference between Japanese and US interest rates, is now showing a loss of $38k due to the change in FX rates. Given the signals that are coming from Japan, this may just be the start of a reversal in USD/JPY rates that could continue for the foreseeable. In this example we used a $1m investment, however the total market for the Yen carry trade is by some estimates into the trillions of USD.

As is often the case, once traders started to unwind their positions, it caused a cascade effect and losses started to mount. For those that had taken their Yen loans and used them to invest in stocks and the equity markets instead of the safer bond market, they now needed to liquidate those stocks in order to repay the Yen loans before their P&L decreased even further. In part, this is what has been suggested caused the global selloff in equities at the beginning of August.

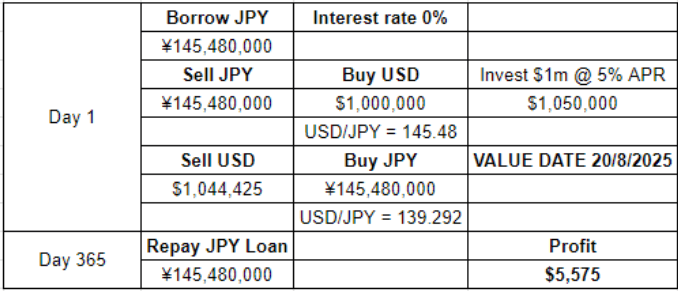

So how might hedging have prevented these losses? Well much like base metals, foreign currencies can be hedged well into the future. Investors are able to hedge foreign exchange risk to match up with payments they are going to make or receive, just like they can if they are buying or selling physical metal in the future.

When hedging FX pairings you do need to consider the forward curve for those rates, much like you would consider the forward curve on metals. It is this forward curve that dictates the FX rates you receive when you are transacting for time periods further out than spot, which could be one week, one month, or a year from today. A negative forward rate means that you will receive a lower rate in the future vs. spot rates, and vice versa for a positive forward rate. The forward curve for FX rates is largely dictated by the difference in interest rates between the two countries. In the case of USD/JPY, the forward rates (or points as they are known) are negative since the US interest rate is much higher than the Japanese rate. For example, on 20th August 2024, the spot rate for USD/JPY was 145.48, however, if you wanted to sell USD and buy JPY with a value date of 1 year from that date, you would only get a rate of 139.292, a points difference of -618.80.

Now, there is no such thing as a riskless investment. Given the large negative forward points value for a 1-year USD/JPY trade, if an investor were to hedge the currency forward on the same day they made their investment, the difference in FX rate would all but wipe out their profits as shown in the below table.

Hedging FX risk on day of investment

However, a good hedging system is not (or at least shouldn’t be) a static program, companies should be constantly evaluating when, how, and what risks they should mitigate. Let’s say that an investor had already entered into the Yen carry trade at an initial FX rate of 147 in September 2023. They held this position for 10 months and were able to generate a return of 13% from bonds and FX appreciation. If at that point, they had entered into a forward FX hedge, they would have secured their investment from any future downside to the USD/JPY rate and locked in the below profit.

Hedging FX risk on day 300

By not hedging their FX risk at that point, they faced unnecessary downside exposure to the FX rate and at the beginning of August watched their profit crash. If they still took no action on the FX rate, their return would still be at the mercy of the markets when they go to repay their Yen loan in September 2024. Using rates at the time of writing they would instead be looking at the below profit of $36k, a decrease in profit of almost $100k from where their position was just a few weeks ago, with no guarantee it won’t reduce further.

Not hedging FX risk at all

Traders often fall into the trap of assuming good things will never end, especially when the good times have lasted for a long time, but when they eventually do, the losses can be catastrophic. Where risks can be mitigated, it is often wise to do so for at least some portion of an investment. A bit like insurance, you don’t particularly like paying it, but you sure are glad to have it when you need it.

As you can see, understanding hedging is not just applicable to base metal trading, it is applicable across all kinds of financial investments. Improving your hedging knowledge is key not just for your career, but potentially for your personal investments as well.